if you didn't have enough credit history, you wouldn't have a high score.

Keep telling yourself that, champ.

follow_along_with_video_below_to_see_how_to_install_our_site_as_web_app

Note: this_feature_currently_requires_accessing_site_using_safari

if you didn't have enough credit history, you wouldn't have a high score.

They're going to check your credit score regardless to approve you for any loan. Why don't you finance it as an auto loan and pay whatever amount you want out of savings as the down payment?

Keep telling yourself that, champ.

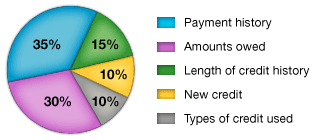

I stand corrected, it's only about 15% of a credit score

if you didn't have enough credit history, you wouldn't have a high score.

Keep telling yourself that, champ.

SFMoto / USAA / Chase all declined my high 700s credit score for a $4,500 loan due to lack of credit history.

SFMoto was trying to sell me the bike, they checked with several of their loan agencies.

USAA is a military only bank that is actually pretty superb, that and they know that military personnel have a fixed income and have to stay financially responsible otherwise they get in deep shit with their unit.

Chase, well, I had about $55,000 invested with them and a hair over $15k in checking / savings accounts. And I've been a customer of theirs since the age of 16. (started with 1st Chicago bank, who was bought by Bank One, who was bought by Chase)

Yet all three places said the same exact thing when declining me: lack of credit history.

Keep in mind, I was 23, had one credit card, and only one cellphone contract on my record. I've never missed a payment since I hardly ever used my credit card, my cellphone bill was setup for auto-payment, and I lived in government housing where they paid for all my utilities. All my cars were paid for with cash, so this would have been the first loan I've ever gotten. I checked my credit score a few months before I bought the bike since I wanted to sort my options out, and it was definitely in the upper 700s (I forget the exact score, haven't checked it since).

SFMoto / USAA / Chase all declined my high 700s credit score for a $4,500 loan due to lack of credit history.

SFMoto was trying to sell me the bike, they checked with several of their loan agencies.

USAA is a military only bank that is actually pretty superb, that and they know that military personnel have a fixed income and have to stay financially responsible otherwise they get in deep shit with their unit.

Chase, well, I had about $55,000 invested with them and a hair over $15k in checking / savings accounts. And I've been a customer of theirs since the age of 16. (started with 1st Chicago bank, who was bought by Bank One, who was bought by Chase)

Yet all three places said the same exact thing when declining me: lack of credit history.

Keep in mind, I was 23, had one credit card, and only one cellphone contract on my record. I've never missed a payment since I hardly ever used my credit card, my cellphone bill was setup for auto-payment, and I lived in government housing where they paid for all my utilities. All my cars were paid for with cash, so this would have been the first loan I've ever gotten. I checked my credit score a few months before I bought the bike since I wanted to sort my options out, and it was definitely in the upper 700s (I forget the exact score, haven't checked it since).

OK? I bought my M3 and 3 months later bought my house with very little credit. Credit history is part of your credit score, and then there's debt to income ratio.

This is where that 'obscure' chart is from... http://www.myfico.com/CreditEducation/WhatsInYourScore.aspx

And what are you trying to argue? I had stated that credit history is important, but then found that article that stated it was only about 15% of the score... So maybe that 15% was enough to screw you over in finding a loan?

I called my credit union and said, I want a loan for this car. They called back the next day and said the money was in your account.wait, youve done this before for that turd car i sold you...

what did you end up doing?